Taxation on Mutual Funds in India

When you redeem mutual fund units and earn a profit, that profit is called a capital gain. How it is taxed depends on two things —

the type of fund and how long you stayed invested.

Types of Capital Gains

Short-Term Capital Gain (STCG)

Short-Term Capital Gain (STCG) arises when you redeem before the qualifying holding period. Taxed at a higher rate.

Long-Term Capital Gain (LTCG)

Long-Term Capital Gain (LTCG) arises when you redeem after the qualifying holding period. Taxed at a lower rate. For equity funds, the first ₹1.25 lakh of LTCG every financial year is completely tax-free.

Taxation by Fund Type

Equity Funds

Large-cap, mid-cap, flexi-cap, index funds, sector funds. Held under 12 months — STCG taxed at 20%. Held 12 months or more — LTCG taxed at 12.5% after ₹1.25 lakh exemption. *₹1.25 lakh LTCG exemption applies to equity funds and equity-oriented funds only*

Debt Funds

Bonds, government securities, fixed-income instruments. All gains, regardless of holding period, are added to your income and taxed at your applicable slab rate. No LTCG benefit available.

What is a Slab Rate?

A slab rate is the income tax rate applicable to you based on your total annual income. In India, income tax is not charged at a flat rate for everyone — it increases progressively as your income rises. The more you earn, the higher the rate at which your income is taxed.

So, when we say debt fund gains are taxed at your slab rate, it simply means the profit from your debt fund is added to your total income for the year and taxed at whatever rate applies to your income bracket — anywhere between 5% and 30%.

How Mutual Fund Investors Can Save Tax

Mutual funds offer market-linked growth along with real tax advantages — if you invest with a plan.

Lower Tax on Long-Term Gains:

Equity mutual funds held for more than 12 months are taxed at 12.5%, which is much lower compared to fixed deposit interest taxed as per your income slab (up to 30%). Staying invested longer helps reduce your overall tax burden while allowing wealth to grow.

₹1.25 Lakh Tax-Free Gains:

Long-term capital gains up to ₹1.25 lakh per financial year are completely tax-exempt. Investors can strategically redeem gains up to this limit each year and reinvest the amount to lock in profits without paying any tax.

SIPs Improve Tax Efficiency:

Each SIP instalment is treated as a separate investment with its own holding period. Over time, more units qualify as long-term, making them eligible for lower tax rates. This makes SIPs not only a disciplined investment approach but also tax-efficient in the long run.

Set Off and Carry Forward Losses:

Capital losses from mutual funds can be used to offset gains and reduce tax liability. Short-term losses can be adjusted against both short-term and long-term gains, while long-term losses can be set off against long-term gains. Unused losses can be carried forward for up to 8 years, offering flexibility in tax planning.

Use Systematic Withdrawal Plan (SWP) Smartly:

A Systematic Withdrawal Plan allows you to withdraw a fixed amount periodically. Since each withdrawal includes both capital and gains, the taxable portion is often lower, helping you manage tax liability efficiently while maintaining regular cash flow.

Hold Investments for the Long Term:

Frequent buying and selling may lead to short-term capital gains, which are taxed at higher rates. Holding investments for the long term ensures eligibility for lower tax rates and helps maximize post-tax returns.

ITR Filing Deadlines (effective 1 April 2026)

For most investors — salaried individuals and those with capital gains or other income — the ITR due date is 31 July. Those with business or professional income where accounts are not required to be audited must file by 31 August. Taxpayers whose accounts must be audited, including companies, have until 31 October.

If you discover an error after filing, you can revise your return anytime up to 31 March of the following year — a full 12-month window.

Frequently Asked Questions

Is Section 80C abolished?

No. It has been renumbered to Section 123 under the Income Tax Act, 2025 (effective April 2026). The ₹1.5 lakh limit and all qualifying instruments — PPF, NSC, life insurance premiums, home loan principal repayment, and others — remain completely unchanged.

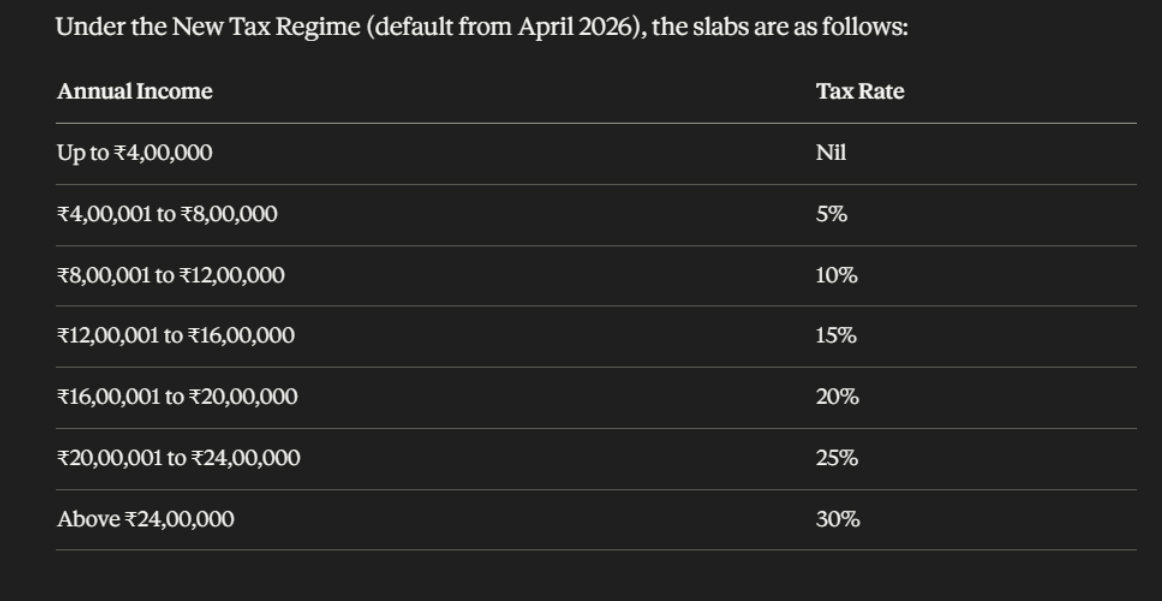

Should I choose the Old or New Tax Regime?

The New Regime (default) offers a higher basic exemption of ₹4 lakh but does not allow most deductions. The Old Regime works better if your total deductions are significant. It is advisable to compare both options before filing your return.

Has the LTCG exemption on equity mutual funds changed?

No. The ₹1.25 lakh per year exemption continues. Gains above this threshold are taxed at 12.5% with no indexation benefit.

Are SIP investments taxed differently?

Each instalment is treated as a separate investment with its own holding period. On redemption, units held over 12 months attract long-term capital gains tax and recent units attract short-term capital gains tax. A single redemption can contain both components.

Is switching between schemes taxable?

Yes. A switch is treated as a redemption and a fresh purchase. Capital gains tax applies based on how long the original units were held, including switches between different plans or options within the same fund house.

Can I set off capital losses?

Yes. Short-term losses can be set off against both short-term and long-term gains. Long-term losses can only be set off against long-term gains. Unused losses can be carried forward for up to 8 years provided the return is filed on time.